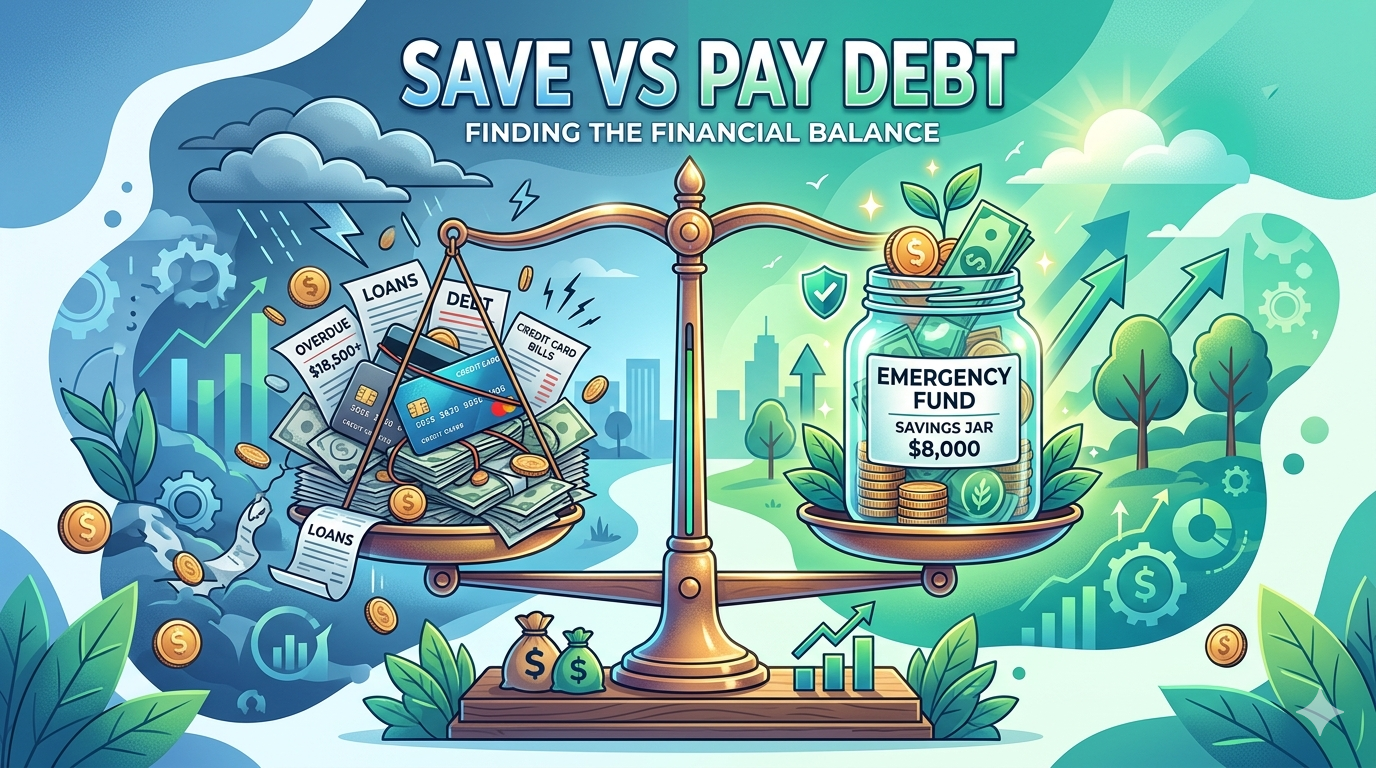

Emergency Fund vs Paying Off Debt: What Should You Do First?

One of the most common personal finance debates is whether to build an emergency fund or pay off debt first. Financial experts disagree on this and both sides have valid arguments. The right answer depends on your specific situation — your interest rates, job stability, and psychological relationship with money.

The Case for Emergency Fund First

Without an emergency fund, any unexpected expense forces you back into debt — undoing your payoff progress. A small $1,000 emergency fund acts as a buffer that keeps you from adding new debt while paying off old debt. Dave Ramsey’s Baby Steps approach recommends this $1,000 starter emergency fund before any aggressive debt payoff. Read our guide on How to Create a Debt Payoff Plan for the complete framework.

The Case for High-Interest Debt First

If you carry credit card debt at 24 percent interest, every dollar in savings earning 4 to 5 percent is costing you 19 to 20 percent net. Mathematically, paying off high-interest debt first is like earning a guaranteed 24 percent return on your money. For high-interest debt, the math strongly favors debt payoff over saving.

The Balanced Approach That Works Best

Build a small starter emergency fund of $500 to $1,000. Then aggressively pay high-interest debt using the strategies in our guide on Debt Snowball vs Debt Avalanche. Once high-interest debt is eliminated, build a full 3 to 6 month emergency fund. Then tackle lower-interest debt.

Conclusion

Start with a small emergency fund to prevent new debt, then attack high-interest debt aggressively, then build a full emergency fund. This balanced approach protects against setbacks while minimizing the interest cost of carrying high-rate