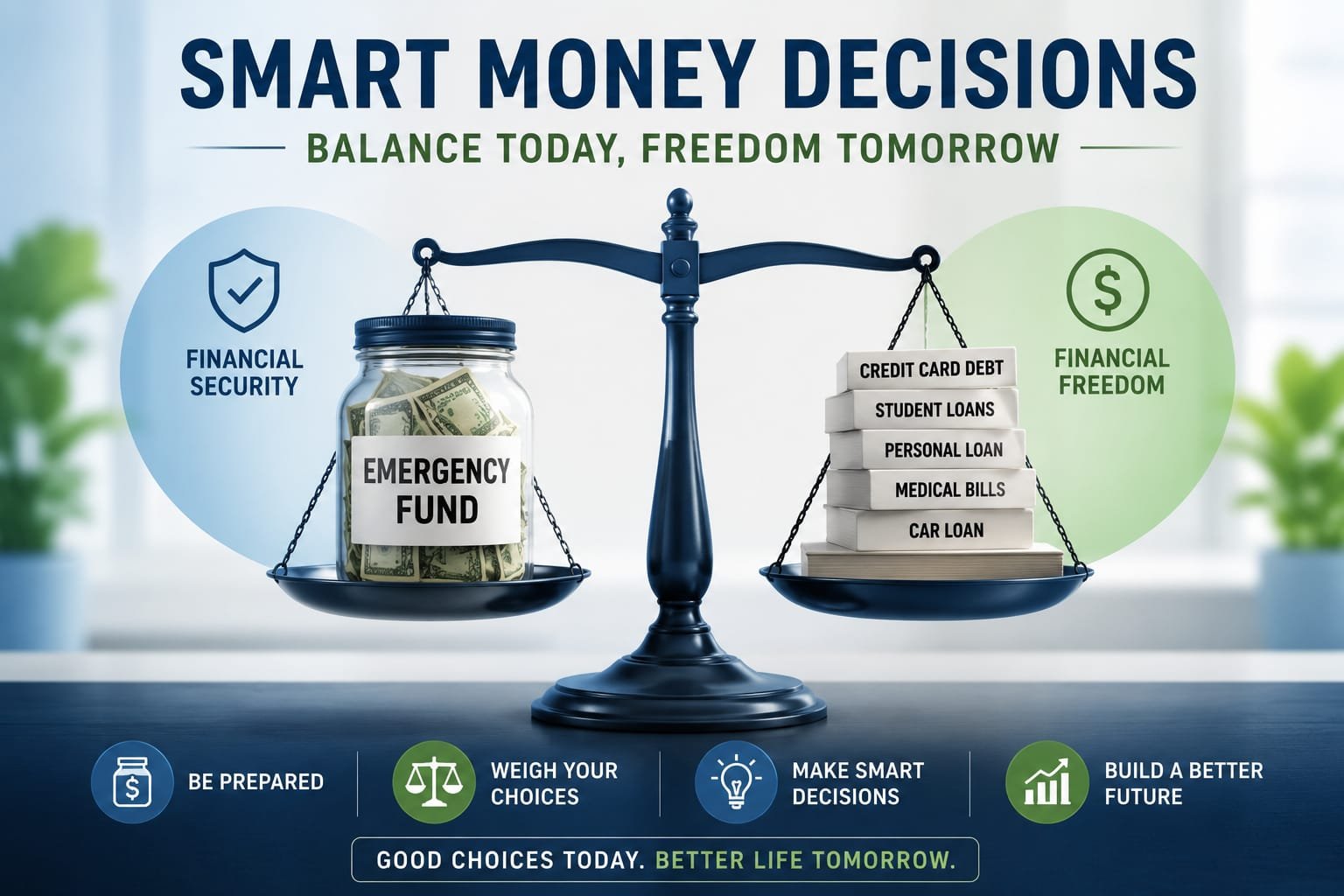

Emergency Fund vs Paying Off Debt: How to Make the Right Decision for Your Situation

Should you build an emergency fund or pay off debt first? This question sits at the intersection of personal finance math and personal finance psychology — and the technically correct answer for one person may be the practically wrong answer for another. Personal finance experts have debated this question for decades, with Dave Ramsey advocating for a starter emergency fund before debt payoff and many mathematically-oriented advisors recommending high-interest debt elimination before saving. This guide helps you navigate the real answer based on your specific situation.

Disclaimer: This content is for educational purposes only and does not constitute financial advice. Individual financial situations vary significantly. Consult a qualified financial advisor for personalized guidance.

The Core Tension — Why This Question Is Genuinely Difficult

The emergency fund versus debt payoff tension exists because both sides have compelling logic. The mathematical case for paying high-interest debt first is clear: money sitting in a savings account earning 4 to 5 percent while you carry credit card debt at 22 percent is costing you a net 17 to 18 percent annually. Every dollar in savings instead of debt payoff is a negative return investment.

But the practical case for emergency fund first is equally compelling: without any emergency buffer, every unexpected expense — a car repair, a medical bill, a home maintenance issue — forces you back into debt, potentially undoing months of payoff progress. People who carry no emergency buffer while aggressively paying debt often find themselves in a frustrating cycle of paying down debt and then rebuilding it with each life disruption.

The resolution of this tension depends on factors specific to your situation. For context on how this fits into a complete debt elimination strategy, read our guide on Debt Snowball vs Debt Avalanche.

The Mathematical Case for Paying High-Interest Debt First

The pure mathematics strongly favor paying high-interest debt before building savings for anyone carrying credit card debt at typical rates. Here is the arithmetic: a dollar in a high-yield savings account in 2026 earns approximately 4 to 5 percent annually. A dollar applied to a credit card balance at 22 percent saves you 22 percent in interest. The net advantage of paying down the credit card is 17 to 18 percent annually — a guaranteed, risk-free return better than virtually any investment.

Over a year, keeping $5,000 in savings at 5 percent while carrying $5,000 in credit card debt at 22 percent costs you approximately $850 in net interest — money that could have been used to reduce your balance. Over two years, this cost compounds further. The mathematically optimal strategy eliminates high-interest debt as fast as possible while keeping savings minimal.

The Practical Case for Emergency Fund First

Despite the mathematical case for debt-first, the practical reality of most people’s financial lives makes some emergency savings essential before aggressive debt payoff. The disruption cycle is the key risk: if you carry no buffer and an unexpected $800 car repair arrives while you are aggressively paying down credit cards, you are forced to charge the repair — wiping out multiple months of payoff progress in one event.

Research on financial behavior consistently shows that people without emergency funds are more likely to abandon debt payoff plans because they experience these disruptions as evidence that their plan is not working. The psychological damage to motivation from repeated setbacks is a real cost that does not appear in the mathematical calculation.

A small emergency fund acts as a financial shock absorber that keeps your debt payoff plan intact through the inevitable disruptions of real life. This is the core insight behind Dave Ramsey’s recommendation of a $1,000 starter emergency fund before beginning aggressive debt payoff — not because $1,000 covers everything, but because it covers most common emergencies and prevents the disruption cycle.

How Your Interest Rates Should Guide the Decision

Your specific interest rates are the most important quantitative factor in this decision.

If you carry credit card debt at 18 percent or higher: The mathematical case for prioritizing debt payoff is overwhelming. Build a small starter emergency fund of $1,000 to $2,000, then direct every available dollar to the highest-interest debt until eliminated.

If your debt is at 8 to 15 percent (personal loans, auto loans, student loans): The gap between debt interest and savings returns is smaller. A more balanced approach — building a 1 to 2 month emergency fund while making above-minimum debt payments — makes more sense.

If your debt is at 3 to 7 percent (mortgages, subsidized student loans): The mathematical advantage of debt payoff over savings is minimal or absent. Building a full emergency fund while making standard debt payments is entirely reasonable and may be preferable.

How Income Stability Affects the Decision

Income stability is a crucial factor that changes the optimal balance between emergency fund and debt payoff. With stable, predictable income: a smaller emergency fund is lower risk because your next paycheck reliably arrives on schedule. With variable or uncertain income (freelancers, commission earners, contract workers, small business owners): a larger emergency fund is more critical because income disruptions are more likely and less predictable.

If you are in a stable salaried position with no significant job security concerns, a $1,000 to $2,000 starter emergency fund before aggressive debt payoff is reasonable. If your income is variable or your job situation has significant uncertainty, building a larger buffer of 2 to 3 months of expenses before aggressive debt payoff better protects your plan from income disruptions.

The Balanced Approach — What Most Financial Advisors Actually Recommend

The approach that works best for most people in most situations is a balanced hybrid rather than a pure debt-first or savings-first strategy.

Phase 1: Build a starter emergency fund of $1,000 to $2,000. This covers the majority of common unexpected expenses and prevents the disruption cycle. This phase should take 1 to 3 months depending on your income and current expenses. Do not skip this step — it protects everything that follows.

Phase 2: Attack high-interest debt aggressively. Direct every available dollar above minimum payments to your highest-rate debt using the debt avalanche method. For strategies to accelerate this phase, see our guides on How to Pay Off Credit Card Debt Fast and How to Negotiate With Creditors. Continue this phase until all high-interest debt is eliminated.

Phase 3: Build a full emergency fund of 3 to 6 months of expenses. With high-interest debt gone, the money previously going to debt payoff now goes to building this comprehensive buffer. 3 months is sufficient for most dual-income households or stable single-income situations. 6 months is appropriate for single-income households, variable income situations, or anyone in a field with challenging job markets.

Phase 4: Continue paying remaining lower-interest debt while beginning wealth building — investing in retirement accounts, building additional savings, and working toward financial goals.

What to Do With Your Emergency Fund

Your emergency fund should be liquid — accessible within 1 to 2 business days without penalty. High-yield savings accounts are the standard recommendation: they earn 4 to 5 percent in 2026, are FDIC insured, and accessible when needed. Keep your emergency fund separate from your regular checking account to reduce temptation to spend it on non-emergencies. Do not invest your emergency fund in stocks or other volatile assets — the purpose is stability and accessibility, not growth.

Rebuilding Your Emergency Fund After Using It

When you use your emergency fund for a genuine emergency, rebuilding it immediately becomes the priority before resuming aggressive debt payoff. An emergency fund that is depleted and not replenished provides no protection for the next unexpected expense. Temporarily reduce your extra debt payments to rebuild the emergency fund, then return to aggressive payoff. This discipline — treating emergency fund rebuilding as a financial priority — is what makes the system work long-term.

Frequently Asked Questions

What counts as an emergency fund emergency? Genuine emergencies include job loss, major medical expenses, critical home or car repairs, and family emergencies requiring travel or support. Non-emergencies include sales, vacations, electronics upgrades, and predictable annual expenses that should be budgeted for separately.

Is $1,000 really enough for a starter emergency fund? For most people, $1,000 covers the majority of common unexpected expenses — most car repairs, typical medical copays, minor home repairs, and similar disruptions. It is not sufficient for job loss or major emergencies, but it prevents the most common disruptions that derail debt payoff plans.

Should I use my emergency fund to pay off debt? Generally no. Depleting your emergency fund to pay off debt leaves you with no buffer for unexpected expenses, which typically results in going back into debt when life disrupts your plan.

Conclusion

The emergency fund versus debt payoff question does not have a single universal answer — it has a right answer for your specific interest rates, income stability, and financial psychology. For most people carrying high-interest credit card debt, the balanced approach works best: a starter emergency fund of $1,000 to $2,000 first, then aggressive debt payoff, then a full emergency fund. This approach protects your plan from disruption while still dramatically reducing the interest cost of carrying high-rate debt. Build your complete debt elimination plan with our guides on How to Create a Debt Payoff Plan That Actually Works and Debt Snowball vs Debt Avalanche.