How to Create a Debt Payoff Plan That Actually Works

Most people who decide to get out of debt fail not because they lack motivation but because they lack a realistic plan. Good intentions without a concrete roadmap lead to inconsistent effort and eventual abandonment. This guide walks you through building a debt payoff plan that is specific, realistic, and designed for the way real life actually works.

Disclaimer: This content is for educational purposes only and does not constitute financial advice.

Step 1 — List Every Debt You Have

You cannot fight what you cannot see. Create a complete list of every debt including the creditor name, current balance, interest rate, minimum payment, and due date. Include credit cards, personal loans, medical debt, student loans, car loans — everything. Many people discover debts they had mentally minimized once they write everything down. This honest accounting is the foundation of your plan.

Step 2 — Know Your Numbers

Calculate your total monthly income after taxes. List every monthly expense in detail. The difference between income and expenses is your potential debt payment amount. If expenses exceed income you have a cash flow problem that must be addressed before any debt payoff plan will work. Look for immediate expense reductions — subscriptions to cancel, discretionary spending to cut, and any obvious waste.

Step 3 — Find Your Extra Payment Amount

After covering essential expenses and minimum debt payments, how much is left? This is your accelerated debt payment amount. Even an extra 500 rupees or 10 dollars per month accelerates your payoff significantly over time. If there is nothing left, the plan must include either increasing income through a side hustle or reducing expenses further before progress is possible.

Step 4 — Choose Your Payoff Strategy

Using your debt list, choose either the debt snowball or debt avalanche strategy as your ordering method. List your debts in the chosen order and designate which debt receives your extra payment each month. Every other debt receives only its minimum payment until its turn comes.

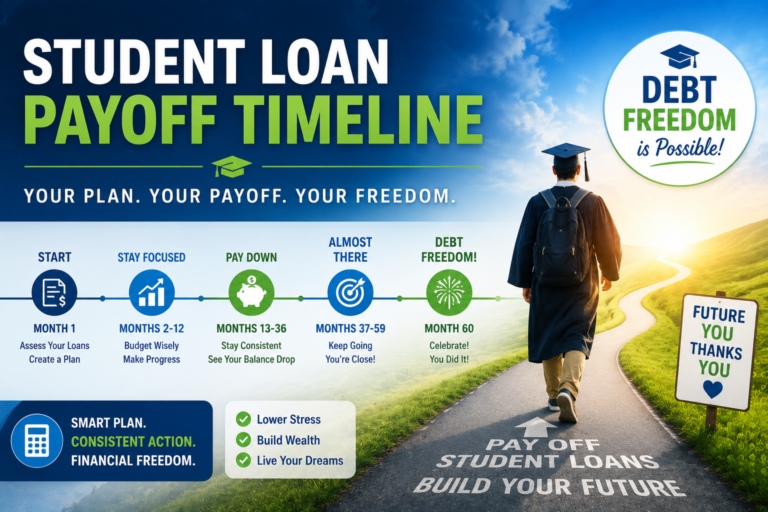

Step 5 — Set a Realistic Target Date

Using a debt payoff calculator, estimate when each debt will be eliminated given your current payment amounts. This gives you a concrete finish line. Adjust your plan if the timeline is discouraging — consider increasing your extra payment amount or finding additional income sources to accelerate the schedule.

Step 6 — Build In Protection Against Setbacks

Life interrupts debt payoff plans — unexpected expenses, income disruptions, emergencies. Build a small emergency fund of one month of expenses before aggressively paying debt. This prevents you from going back into debt every time life happens.

Step 7 — Track and Celebrate Progress

Review your debt balances monthly. Celebrate every debt that reaches zero. Progress tracking keeps motivation high and helps you catch problems early if spending has crept up or income has changed.

Conclusion

A debt payoff plan that works is specific, realistic, and reviewed regularly. List every debt, know your numbers, find extra payment money, choose your strategy, set a target date, protect against setbacks, and track your progress. This six-step process has helped countless people reach zero debt — and it can work for you.